Understanding how to start a Layaway Program begins with knowing what makes it valuable.

A layaway program allows customers to reserve products and pay over time through a structured payment plan, making it easier for them to afford higher-value items without credit.

This model is gaining traction as demand for flexible payments rises. In fact, according to the Federal Reserve, about 15% of U.S. adults used instalment options like BNPL in 2024, reflecting this shift.

In this guide, you will learn how to start a layaway program step by step, from understanding the model to building a practical layaway system setup that works for your business.

Key Takeaways

- A layaway program helps businesses increase sales by offering flexible, debt-free payment options to customers.

- Success depends on a clear layaway system setup, including payment terms, policies, and product selection.

- Understanding legal requirements for layaway programs protects your business and builds customer trust.

- When implemented well, a layaway payment plan improves cash flow, reduces cart abandonment, and boosts customer loyalty.

What Is a Layaway Program and How Does It Work?

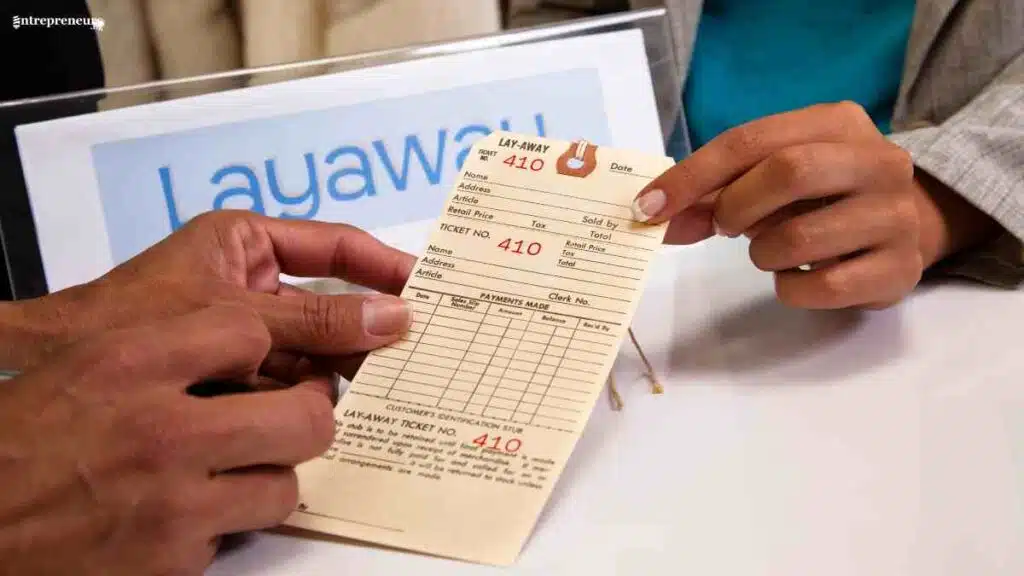

A layaway program is a payment arrangement that allows customers to reserve a product and pay for it over time before taking possession of it.

Unlike credit-based systems, the customer does not receive the item immediately. Instead, the business holds the product until the full payment is completed.

This structure makes a layaway payment plan fundamentally different from financing or buy now, pay later models.

There is no borrowing involved, no interest accumulation, and typically no credit checks. The transaction is simple: the customer commits to buying an item, pays in instalments, and collects it once the agreed amount is fully paid.

How a Layaway Program Works

At its core, a layaway system follows a structured but straightforward process. However, the effectiveness of the system depends on how clearly each step is defined and managed.

Step 1: Customer Selects a Product

The process begins when a customer identifies an item they want to purchase but cannot pay for in full at that moment.

This is common with higher-ticket products such as electronics, furniture, or seasonal goods.

Instead of losing the sale, the business offers the option to place the item on layaway. This immediately reduces hesitation and increases the likelihood of conversion.

Step 2: Initial Deposit Is Made

To secure the item, the customer pays an initial deposit. This deposit serves as a commitment and signals serious intent to complete the purchase.

The amount required varies by business, but it is typically a percentage of the total price.

This step is critical in a layaway system setup because it filters out non-serious buyers and protects the business from unnecessary inventory holding.

Step 3: Payment Plan Is Established

After the deposit, the business and customer agree on a structured payment schedule. This defines how much the customer will pay and how often payments will be made.

The payment plan must be clear, realistic, and documented. It usually includes:

- The total duration of the layaway agreement

- Payment frequency (weekly, bi-weekly, or monthly)

- Minimum payment amounts

This stage is where many businesses either succeed or fail. A poorly designed layaway payment plan can lead to missed payments, cancellations, and operational inefficiencies.

Step 4: Business Holds the Item

Once the agreement is in place, the business removes the item from available inventory and stores it until the payment is completed.

This is a defining feature of how to set up a layaway system. The customer does not take possession yet, which eliminates the risk of default after delivery.

However, it also introduces inventory management considerations, especially for businesses with limited storage or fast-moving products.

Step 5: Customer Makes Instalment Payments

The customer proceeds to make payments according to the agreed schedule. Each payment reduces the outstanding balance until the full amount is paid.

During this phase, communication is essential. Businesses that actively remind customers of upcoming payments and provide flexible options tend to experience higher completion rates.

Step 6: Completion and Product Collection

Once the final payment is made, the transaction is completed, and the customer collects the product.

At this point, the business records the full sale, and the customer receives the item without having incurred debt or interest.

This creates a positive customer experience and often leads to repeat purchases.

Step 7: Handling Defaults or Cancellations

Not all layaway plans reach completion. Some customers may miss payments or decide to cancel.

This is where the legal requirements for layaway programs and internal policies become important. Most businesses include terms that specify:

- Whether deposits are refundable

- Any cancellation fees

- Time limits before an order is forfeited

A well-defined policy ensures fairness while protecting the business from losses.

Layaway Program Process at a Glance

| Stage | What Happens | Business Benefit | Customer Benefit |

|---|---|---|---|

| Product Selection | Customer chooses item | Captures interest | Access to desired product |

| Deposit Payment | Initial commitment made | Reduces risk | Secures item |

| Payment Plan Setup | Terms agreed | Predictable cash flow | Flexible payments |

| Item Storage | Business holds product | Prevents loss | Guaranteed availability |

| Instalment Payments | Gradual payments made | Ongoing revenue | Budget-friendly purchase |

| Final Payment | Balance completed | Full sale realised | Ownership without debt |

| Collection | Customer receives item | Completed transaction | Product acquired |

Why Understanding How Layaway Works Is Important

Understanding how a layaway program works is not just about mechanics. It is about designing a system that balances flexibility with control.

Businesses that take the time to structure their layaway system setup properly often see improved sales performance, better customer relationships, and more predictable revenue streams.

On the other hand, a poorly executed system can lead to inventory bottlenecks, payment defaults, and customer dissatisfaction.

That is why mastering the fundamentals of how to set up a layaway system is the foundation for building a program that truly works.

Layaway vs Credit vs BNPL

Understanding the difference between layaway, traditional credit, and Buy Now Pay Later (BNPL) is essential when deciding how to structure your payment options.

While all three models aim to make purchases more accessible, they operate very differently in terms of risk, cash flow, and customer experience.

Choosing the right one or combining them strategically can significantly impact your sales and customer trust.

| Feature | Layaway | Credit (e.g., Credit Cards/Loans) | Buy Now Pay Later (BNPL) |

|---|---|---|---|

| Product Delivery | After full payment | Immediate | Immediate |

| Payment Structure | Instalments before receiving item | Pay later with interest | Instalments after receiving item |

| Interest Charges | None | Usually high interest | Often interest-free (short-term) |

| Credit Check Required | No | Yes | Sometimes (varies by provider) |

| Risk to Business | Low (item retained until paid) | Medium (depends on lender) | Low (provider pays merchant upfront) |

| Risk to Customer | Low (no debt accumulation) | High (can lead to debt) | Medium (missed payments incur fees) |

| Ownership Timing | After full payment | Immediate | Immediate |

| Best For | Budget-conscious buyers | Customers needing financing | Convenience-driven shoppers |

| Cash Flow for Business | Gradual | Immediate (via lender) | Immediate (via BNPL provider) |

In simple terms, a layaway program is the safest option for both businesses and customers who want to avoid debt.

Credit, on the other hand, offers instant ownership but comes with financial risk due to interest.

BNPL sits in the middle, combining convenience with speed, but still exposes customers to potential fees if payments are missed.

How to Start a Layaway Program in 10 Easy Steps

Starting a layaway program does not have to be complicated, but it does require a clear structure and intentional planning.

When done right, it can become a powerful tool to increase sales, improve customer loyalty, and offer flexible payment options without exposing your business to unnecessary risk.

Below, you will learn how to start a layaway program step by step, using a simple framework that works for both retail and e-commerce businesses.

Step 1: Understand the Layaway Business Model

Before you begin any layaway system setup, you need to fully understand how the layaway model works from a business perspective.

This step is not just theoretical. It shapes every decision you will make, from pricing to policy design and customer communication.

At its core, a layaway program is built on a simple principle: customers commit to a purchase, pay in instalments, and receive the product only after completing payment.

Unlike credit or BNPL, this model keeps control firmly in your hands because the item remains in your inventory until it is fully paid for.

A strong foundation at this stage ensures that your layaway payment plan is both customer-friendly and financially sustainable.

Key Elements of the Layaway Business Model

| Element | What It Means | Why It Matters |

|---|---|---|

| Payment Before Ownership | Customer pays fully before receiving item | Eliminates credit risk |

| Inventory Retention | Business holds the product during payment period | Protects against default |

| Structured Instalments | Payments spread over time | Makes products more accessible |

| No Interest | No borrowing involved | Appeals to debt-averse customers |

| Policy-Driven System | Clear rules guide the process | Prevents disputes and confusion |

When you understand these core elements, it becomes easier to design a system that works in real life, not just on paper.

More importantly, it positions you to build a layaway program that aligns with your business goals while meeting customer expectations.

Step 2: Choose the Right Products for Your Layaway Program

Once you understand the layaway model, the next step is to decide which products to include in your programme.

Not every item in your inventory is suitable for a layaway payment plan, so careful selection is essential to ensure profitability and smooth operations.

In most cases, layaway works best for products that customers want but may struggle to pay for upfront.

These are typically higher-value items or products tied to specific occasions. By offering such items on layaway, you remove a major buying barrier and make the purchase feel more manageable.

Product Selection Criteria for Layaway

| Criteria | What It Means | Importance |

|---|---|---|

| High-Value Items | Products with higher price points | Encourages customers to use instalments |

| Durable Goods | Non-perishable, long-lasting items | Safe to hold over time |

| Consistent Demand | Items with steady interest | Reduces risk of unsold stock |

| Storage Feasibility | Easy to store without damage | Prevents inventory issues |

| Seasonal Relevance | Products tied to events or holidays | Drives timely sales |

Choosing the right products is a strategic decision.

When done properly, it increases conversion rates, reduces cancellations, and ensures your layaway program remains efficient and profitable.

Step 3: Set Payment Terms and Duration

After selecting the right products, the next step is to define how customers will pay for them. This is where your layaway program starts to take real shape.

Clear and realistic payment terms are essential because they directly affect customer commitment, completion rates, and your overall cash flow.

If the terms are too strict, customers may drop out. If they are too loose, you risk delays, defaults, and inventory being tied up for too long.

Key Payment Terms to Define

| Element | What It Involves | Best Practice |

|---|---|---|

| Initial Deposit | Upfront payment to secure the item | Typically 10%–30% of product price |

| Payment Frequency | How often customers pay | Weekly or monthly for simplicity |

| Payment Amount | Minimum instalment size | Keep it affordable but meaningful |

| Duration | Total time to complete payment | 4–12 weeks depending on product value |

| Grace Period | Extra time for missed payments | Offer limited flexibility to reduce cancellations |

Setting these terms correctly is critical to how to set up a layaway system that works in practice.

When customers clearly understand what is expected, they are more likely to complete their payments.

At the same time, your business maintains control over cash flow and inventory, ensuring the layaway program remains efficient and sustainable.

Step 4: Create a Clear Layaway Policy

With your payment terms defined, the next step is to formalise everything into a clear and structured layaway policy.

This is one of the most important parts of a layaway program because it protects your business while setting the right expectations for customers.

Your policy should be simple, transparent, and easy for customers to understand. At the same time, it must address key operational and legal considerations, especially around cancellations, refunds, and missed payments.

Key Components of a Layaway Policy

| Component | What It Covers | Importance |

|---|---|---|

| Payment Terms | Deposit, instalments, and duration | Sets clear expectations |

| Cancellation Rules | Conditions for cancelling orders | Prevents disputes |

| Refund Policy | Whether deposits are refundable | Protects your revenue |

| Payment Deadlines | Due dates and grace periods | Keeps payments on track |

| Storage Terms | How long items are held | Manages inventory efficiently |

| Default Handling | What happens if payments stop | Reduces business risk |

A well-crafted layaway policy does more than enforce rules. It builds trust.

Customers are more likely to commit when they understand exactly how the process works and what happens in different scenarios.

For your business, it creates a system that runs smoothly, even as your layaway program scales.

Step 5: Determine Fees and Pricing Strategy

Once your policy is in place, the next step is to decide whether you will charge any fees and how your pricing will support the sustainability of your layaway program.

While a layaway payment plan is typically interest-free, many businesses introduce small fees to cover administrative costs, storage, and the risk of cancellations.

However, these fees must be reasonable. If they feel excessive, they can discourage customers from using the service altogether.

Your pricing strategy should also account for the fact that inventory will be tied up for a period. This means you need to ensure your margins can absorb delayed full payment while still maintaining healthy cash flow.

Key Pricing and Fee Considerations

| Element | What It Involves | Best Practice |

|---|---|---|

| Service Fee | Small charge for managing layaway | Keep it low or optional to encourage uptake |

| Cancellation Fee | Deduction if customer cancels | Use to offset holding costs |

| Late Payment Fee | Penalty for missed deadlines | Apply moderately to maintain discipline |

| Product Pricing | Base price of item | Maintain standard pricing to stay competitive |

| Discounts | Incentives for early completion | Encourage faster payments and turnover |

A thoughtful approach to fees and pricing ensures your layaway system setup remains attractive to customers while still working for your business financially.

The goal is not to maximise fees, but to create a fair structure that supports both parties and keeps the programme running efficiently.

Step 6: Choose the Right Tools or Software

At this stage, your layaway program needs a system to run efficiently.

Whether you operate a physical store or an online business, choosing the right tools is essential for tracking payments, managing inventory, and keeping everything organised.

A manual system may work when you are just starting out. However, as your layaway program grows, it can quickly become difficult to manage without proper support.

Tool Options for Managing a Layaway Program

| Tool Type | What It Does | Best For |

|---|---|---|

| Point of Sale (POS) Systems | Tracks payments and manages orders in-store | Retail businesses |

| E-commerce Platforms | Enables layaway or instalment features online | Online stores |

| Payment Tracking Software | Monitors instalments and balances | Small businesses starting out |

| Accounting Tools | Records transactions and reconciles payments | Financial management |

| CRM Systems | Manages customer communication and reminders | Customer retention |

Choosing the right combination of tools depends on your business size and model. For a small business, a simple spreadsheet combined with a payment tracker may be enough at the beginning.

However, for larger operations or e-commerce stores, automated systems are more effective.

Step 7: Train Staff or Automate the Process

With your tools in place, the next step is to ensure your layaway program runs smoothly on a day-to-day basis.

This comes down to either training your team effectively or setting up automation where possible. Without this, even the best-designed layaway system setup can break down during execution.

If you run a physical store, your staff must understand every aspect of the layaway payment plan.

They should be able to explain the process clearly to customers, handle payments accurately, and enforce your policy consistently.

Staff Training vs Automation in Layaway Systems

| Approach | What It Involves | Best Use Case |

|---|---|---|

| Staff Training | Educating employees on policies, payments, and customer communication | Physical retail stores |

| Payment Reminders | Automated alerts for upcoming or missed payments | Ecommerce and hybrid businesses |

| Order Tracking | System updates on payment progress and order status | All business types |

| Customer Support | Handling enquiries and resolving issues | Both manual and automated setups |

| Workflow Automation | End-to-end system handling of layaway process | Scaling businesses |

Whether you choose manual management, automation, or a mix of both, the goal remains the same: consistency and clarity.

Customers should have a smooth experience from start to finish, and your business should operate without unnecessary friction.

When this step is done right, your layaway program becomes easier to manage and more reliable as it grows.

Step 8: Launch Your Layaway Program

After setting up your system, policies, and processes, the next step is to officially launch your layaway program.

This is where everything comes together and becomes visible to your customers. A well-executed launch ensures that your efforts translate into actual usage, not just a feature sitting unnoticed.

Launching a layaway program is more than simply announcing it. You need to position it clearly as a valuable payment option that solves a real problem for your customers.

If customers do not understand how it works or why it benefits them, adoption will be slow.

Key Elements of a Successful Launch

| Element | What It Involves | Importance |

|---|---|---|

| Clear Messaging | Explain how the layaway program works | Reduces confusion and builds trust |

| In-Store Visibility | Signage and staff communication | Encourages immediate adoption |

| Website Integration | Dedicated page or checkout option | Makes it accessible for online customers |

| Simple Onboarding | Easy steps to start a layaway plan | Improves customer experience |

| Policy Transparency | Display terms clearly | Prevents misunderstandings |

A strong launch creates momentum. It helps customers quickly see the value of your layaway payment plan and encourages early adoption.

When done right, this step sets the tone for how your program will perform in the long run and ensures your layaway system setup delivers real business results.

Step 9: Promote and Market Your Layaway Program

Launching your layaway program is only the beginning. To see real results, you need to actively promote it so customers know it exists and understand how it benefits them.

Even the best layaway system setup will underperform if it is not visible or clearly communicated.

Marketing your layaway payment plan should focus on one core message: affordability without debt.

Customers are more likely to engage when they see it as a practical solution to their financial constraints rather than just another payment option.

Key Channels for Promoting Your Layaway Program

| Channel | What It Involves | Importance |

|---|---|---|

| In-Store Promotion | Posters, signage, and staff recommendations | Captures walk-in customers |

| Website Placement | Highlight on homepage and product pages | Increases online visibility |

| Social Media | Posts showcasing flexible payment options | Drives awareness and engagement |

| Email Marketing | Campaigns explaining benefits and how it works | Educates and converts existing customers |

| Checkout Messaging | Reminder at point of purchase | Reduces hesitation and boosts conversions |

Effective promotion turns your layaway program into a competitive advantage.

When customers consistently see and understand the option, they are more likely to choose it, complete their purchases, and return for future transactions.

Step 10: Monitor, Evaluate, and Optimise Your Layaway Program

Once your layaway program is up and running, the final step is to continuously monitor its performance and make improvements where necessary.

This is what separates a functional system from a truly successful one. Without regular evaluation, small issues can grow into bigger problems that affect both customer experience and profitability.

At this stage, you need to pay close attention to how customers interact with your layaway payment plan.

Are they completing their payments on time? Are there frequent cancellations? Is inventory being held for too long? These insights will help you refine your approach and strengthen your layaway system setup over time.

Key Metrics to Track and Improve

| Metric | What It Measures | Importance |

|---|---|---|

| Completion Rate | Percentage of customers who finish payments | Indicates programme success |

| Cancellation Rate | Number of cancelled layaway orders | Highlights policy or pricing issues |

| Payment Timeliness | How often payments are made on schedule | Reflects customer engagement |

| Inventory Holding Time | How long items are reserved | Affects stock availability |

| Customer Feedback | Customer satisfaction and experience | Guides improvements |

By consistently reviewing these metrics, you can identify what is working and what needs adjustment.

You may need to tweak your payment terms, update your policies, or improve communication with customers.

How to Create a Winning Layaway Policy

A layaway program is only as strong as the policy behind it.

While your payment structure and tools determine how the system operates, your policy defines the rules that protect your business and guide your customers.

Without a clear policy, misunderstandings become inevitable, and disputes can quickly erode trust.

Key Elements of a Strong Layaway Policy

A well-crafted layaway policy typically includes clearly defined payment terms, timelines, and consequences for non-compliance.

It also outlines what happens if a customer cancels or fails to complete payments.

| Policy Element | What It Should Cover |

|---|---|

| Deposit Requirement | Minimum upfront payment |

| Payment Schedule | Frequency and amount of instalments |

| Duration | Timeframe to complete payments |

| Cancellation Terms | Conditions for cancelling orders |

| Refund Policy | Whether payments are refundable |

| Late Payments | Penalties or grace periods |

| Default Terms | What happens if payments stop |

| Collection Timeline | When item must be picked up |

When these elements are clearly defined, your layaway system setup becomes easier to manage and more reliable.

Customers know exactly what to expect, and your team can enforce the rules consistently.

Layaway Policy Sample

Below is a realistic, professionally structured layaway policy that businesses can adapt for their own use.

Made For You Layaway Policy

Thank you for choosing our layaway payment plan. Our layaway program is designed to make your purchases more affordable and convenient.

Please review the terms below carefully before placing an item on layaway.

1. Layaway Eligibility

Layaway is available on selected items only. Eligible products will be clearly marked in-store or online.

2. Initial Deposit

To secure your item, a minimum deposit of 20% of the total purchase price is required at the time of checkout.

This deposit confirms your commitment to the purchase.

3. Payment Schedule

The remaining balance must be paid in instalments based on the agreed plan:

- Payment duration: Up to 8 weeks

- Payment frequency: Weekly or bi-weekly

- Minimum instalment: Determined at checkout

All payments must be completed within the agreed timeframe.

4. Product Holding

All layaway items will be reserved and held by us until full payment is received. Items will not be released or delivered until the balance is fully paid.

5. Payment Methods

We accept the following payment methods for layaway plans:

- Cash

- Debit/credit cards

- Online payments (where applicable)

6. Late Payments

If a scheduled payment is missed:

- A grace period of 3 days may be allowed

- Late payments beyond this period may incur a late fee

Failure to make payments may result in cancellation of your layaway plan.

7. Cancellation Policy

Customers may cancel their layaway plan at any time. However:

- A cancellation fee may apply

- Refunds (if applicable) will exclude service or administrative fees

8. Refund Policy

Refunds for cancelled layaway orders will be processed as follows:

- Deposits may be partially refundable

- Processing time: 5–10 business days

9. Default and Forfeiture

If payments are not completed within the agreed timeframe and no communication is received:

- The layaway order may be cancelled

- Payments made may be forfeited or partially refunded, depending on policy terms

- The item will be returned to stock

10. Changes to Orders

Once a layaway agreement is initiated:

- Items cannot be swapped without approval

- Price changes after the agreement do not affect your order

11. Customer Responsibility

By entering a layaway agreement, you agree to:

- Make payments on time

- Keep your contact details updated

- Communicate any issues in advance

12. Policy Updates

We reserve the right to update this layaway policy at any time. Any changes will not affect existing agreements already in progress.

Acknowledgement

By placing an item on layaway, you confirm that you have read, understood, and agreed to these terms.

Tools and Software for Managing a Layaway Program

To run an efficient layaway program, you need the right tools to track payments, manage inventory, and communicate with customers.

While some small businesses may start manually, using software simplifies your layaway system setup, reduces errors, and improves the overall customer experience.

The right tools will help you stay organised, automate processes, and scale your layaway payment plan as your business grows.

| Tool Type | What It Does | Best For | Example Tools |

|---|---|---|---|

| Point of Sale (POS) Systems | Tracks in-store payments and manages layaway orders | Physical retail stores | Square, Lightspeed |

| Ecommerce Platforms | Integrates layaway or instalment options online | Online businesses | Shopify, WooCommerce |

| Payment Tracking Software | Monitors instalments, balances, and due dates | Small businesses and startups | QuickBooks, spreadsheets |

| Accounting Software | Records transactions and manages financial reports | All business types | Xero, FreshBooks |

| CRM Systems | Handles customer data and communication | Growing businesses | HubSpot, Zoho CRM |

| Automation Tools | Sends reminders and updates automatically | Ecommerce and scaling businesses | Zapier, Mailchimp |

Using the right combination of these tools ensures your layaway program runs smoothly from start to finish.

It reduces manual workload, improves accuracy, and helps you deliver a seamless experience that keeps customers engaged and committed to completing their payments.

Legal and Financial Considerations

Setting up a layaway program goes beyond operations and marketing. You must also address key legal and financial considerations to protect your business and maintain customer trust.

A poorly structured system can lead to disputes, regulatory issues, or financial losses, especially as your programme grows.

From a legal standpoint, your layaway policy must comply with consumer protection laws in the regions where you operate.

Understanding these factors early will help you build a layaway system setup that is both compliant and sustainable.

Key Legal Considerations for Layaway Programs

| Area | What It Involves | Importance |

|---|---|---|

| Consumer Protection Laws | Rules governing refunds, cancellations, and transparency | Prevents legal disputes and penalties |

| Clear Terms & Conditions | Written agreement outlining payment terms and obligations | Builds trust and avoids misunderstandings |

| Refund Regulations | Legal requirements on how deposits and payments are handled | Ensures compliance and fairness |

| Data Protection | Handling customer payment and personal data securely | Protects customer privacy and avoids breaches |

| Disclosure Requirements | Clearly stating fees, timelines, and penalties upfront | Avoids misleading customers |

In many countries, businesses are required to clearly disclose all terms before a customer enters a layaway agreement.

This includes payment schedules, refund policies, and any fees. Failing to do so can lead to complaints or legal action.

Key Financial Considerations for Layaway Programs

| Area | What It Involves | Importance |

|---|---|---|

| Cash Flow Management | Receiving payments over time instead of upfront | Requires planning to maintain liquidity |

| Inventory Holding Costs | Storing items until fully paid | Can affect stock turnover |

| Pricing Strategy | Ensuring margins cover delayed payments | Maintains profitability |

| Default Risk | Customers failing to complete payments | May lead to lost time and resources |

| Administrative Costs | Managing payments, tracking, and communication | Impacts overall efficiency |

One of the biggest financial realities of a layaway program is delayed revenue recognition. While you receive payments gradually, the full profit is only realised at the end of the payment cycle.

This means you must plan carefully to avoid cash flow pressure.

Balancing Compliance and Profitability

A successful layaway program finds the balance between legal compliance and financial efficiency. On one hand, you must protect customers with fair and transparent policies.

On the other hand, you must protect your business by managing risk and maintaining profitability.

When both sides are handled properly, your layaway payment plan becomes a reliable system that supports growth rather than creating operational strain.

How to Market Your Layaway Program for Maximum Results

Creating a layaway program is only half the job. To see real impact, you need to market it strategically so customers not only notice it but understand its value.

A well-promoted layaway payment plan can significantly increase conversions, especially among customers who are hesitant due to price constraints.

The key is to position your layaway program as a smart, flexible, and stress-free way to shop, rather than just another payment option. When customers clearly see how it benefits them, adoption becomes much easier.

Positioning Your Layaway Program the Right Way

Before choosing marketing channels, you must get your messaging right. Customers respond better when the value is clear and relatable.

| Message Angle | What It Means | Why It Works |

|---|---|---|

| Affordability | “Pay small amounts over time” | Reduces price resistance |

| No Debt | “No interest, no credit needed” | Appeals to cautious buyers |

| Flexibility | “Choose a plan that suits you” | Feels personalised |

| Security | “Your item is reserved for you” | Builds trust and urgency |

Strong positioning ensures your layaway system setup is not just visible, but compelling.

Use Multiple Channels to Drive Awareness

To maximise results, your layaway program should appear wherever your customers interact with your business.

Consistency across channels reinforces awareness and encourages action.

| Channel | Strategy | Expected Outcome |

|---|---|---|

| Website | Highlight layaway on homepage, product pages, and checkout | Increases online conversions |

| Social Media | Showcase products with instalment options | Drives engagement and interest |

| Email Marketing | Send campaigns explaining how the program works | Educates and nurtures customers |

| In-Store Promotion | Use signage and staff recommendations | Captures walk-in buyers |

| Checkout Messaging | Remind customers at point of purchase | Reduces hesitation |

The more visible your layaway payment plan is, the more likely customers are to use it.

Simplify the Customer Journey

Marketing alone is not enough. Customers must be able to act immediately once they are interested. If your process feels complicated, you will lose potential sales.

Make it easy for customers to:

- Understand how the layaway program works

- Start a plan in a few simple steps

- Track their payments without confusion

A seamless experience reinforces your marketing efforts and improves completion rates.

Create Urgency and Incentives

To drive faster adoption, consider adding subtle incentives that encourage customers to act quickly.

| Strategy | Example | Benefit |

|---|---|---|

| Limited-Time Offers | “Start your layaway today with zero fees” | Encourages immediate action |

| Seasonal Campaigns | Promote during holidays or back-to-school periods | Aligns with buying behaviour |

| Early Completion Rewards | Small discount for finishing payments early | Improves cash flow |

These tactics make your layaway program feel timely and valuable, rather than optional.

Build Trust Through Transparency

Trust is a major factor in whether customers commit to a layaway payment plan. Your marketing should clearly explain:

- How payments work

- What happens if payments are missed

- Any fees or conditions involved

When customers feel informed, they are more confident in choosing your layaway option.

Turn Your Layaway Program into a Growth Engine

When marketed effectively, your layaway program becomes more than a payment option. It becomes a powerful tool for:

- Increasing average order value

- Reducing cart abandonment

- Attracting new customer segments

- Encouraging repeat purchases

The businesses that succeed are those that consistently communicate value, simplify access, and integrate layaway into their overall customer experience.

Real-Life Examples of Successful Layaway Programs

To truly understand the value of a layaway program, it helps to look at how real businesses have used it to drive sales and build customer trust.

From large retailers to small businesses, successful layaway systems are built on simplicity, clear policies, and strong customer demand for flexible payments.

These examples show how different businesses apply layaway strategies in practical ways and the results they achieve.

| Business | How They Use Layaway | Key Strategy | Results |

|---|---|---|---|

| Walmart | Seasonal layaway for electronics, toys, and holiday items | Focus on peak shopping periods with simple terms | Boosts holiday sales and attracts budget-conscious shoppers |

| Kmart | Traditional layaway available year-round | Long-standing layaway system with flexible payment plans | Built strong customer loyalty over decades |

| Sears | Layaway for appliances and big-ticket items | Targets high-value products with structured instalments | Increased accessibility for expensive purchases |

| Small Retail Boutiques | Layaway for fashion and custom items | Personalised payment plans and customer relationships | Higher conversion rates and repeat customers |

| Ecommerce Stores (via Shopify) | Digital layaway through plugins and manual systems | Integrates instalment options into checkout | Reduces cart abandonment and improves online sales |

These examples highlight an important pattern: successful layaway programs are not limited to large corporations.

While companies like Walmart use layaway to drive seasonal demand at scale, smaller businesses use it to create personalised, flexible shopping experiences.

The key takeaway is that the effectiveness of a layaway program depends less on size and more on execution.

Businesses that keep their systems simple, communicate clearly, and align their layaway payment plan with customer needs consistently see better results.

Conclusion

Starting a layaway program is a practical way to make your products more accessible while maintaining control over risk and cash flow.

When you structure it properly, with clear policies, the right tools, and effective marketing, it becomes more than just a payment option.

We want to see you succeed, and that’s why we provide valuable business resources to help you every step of the way.

- Join over 23,000 entrepreneurs by signing up for our newsletter and receiving valuable business insights.

- Register your business today with Entrepreneurs.ng’s Business Registration Services.

- Tell Your Brand Story on Entrepreneurs.ng, let’s showcase your brand to our global audience.

- Need help with your marketing strategy? Get a Comprehensive Marketing and Sales Plan here.

- Sign up for our Entrepreneurs Success Blueprint Programme to learn how to start and scale your business in just 30 days.

- Book our one-on-one consulting and speak to an expert about structuring and growing your business.

- Visit our shop for business plan templates and other valuable resources to guide you.

- Get our Employee-Employer Super Bundle NDA templates to legally protect your business and workforce.

- Advertise your business to over a million entrepreneurs through our different advertising packages.

Frequently Asked Questions (FAQs)

What is a layaway program?

A layaway program is a payment arrangement where customers pay for a product in instalments and receive it only after completing full payment.

How does a layaway program work?

Customers select an item, make a deposit, pay the balance over time, and collect the product once payment is complete.

Is a layaway program the same as Buy Now Pay Later (BNPL)?

No, layaway requires full payment before delivery, while BNPL allows customers to receive the item immediately and pay later.

Can small businesses offer a layaway program?

Yes, small businesses can easily implement a layaway payment plan with simple tools and clear policies.

What types of products are best for layaway?

High-value, durable, and non-perishable items such as electronics, furniture, and fashion products work best.

Do customers pay interest on layaway plans?

No, layaway programs are typically interest-free, making them attractive to budget-conscious customers.

How long should a layaway payment plan last?

Most layaway plans last between 4 to 12 weeks, depending on the product price and business policy.

What happens if a customer misses a payment?

Depending on your policy, you may offer a grace period, charge a late fee, or cancel the layaway agreement.

Are layaway deposits refundable?

This depends on your policy. Some businesses offer partial refunds, while others deduct cancellation fees.

Is a layaway program profitable for businesses?

Yes, when structured properly, it increases sales, improves cash flow, and reduces the risk of non-payment.

Can ecommerce stores offer layaway programs?

Yes, ecommerce businesses can set up layaway systems using plugins, payment tools, or manual tracking methods.

What are the legal requirements for layaway programs?

Businesses must clearly disclose terms, including payment schedules, fees, cancellation policies, and refund conditions.

How do I track layaway payments effectively?

You can use POS systems, accounting software, or payment tracking tools to monitor instalments and balances.

Can customers cancel a layaway plan?

Yes, most businesses allow cancellations, but fees or partial refunds may apply depending on the policy.

How can I encourage customers to use my layaway program?

Promote it clearly, highlight its benefits, and make the process simple and transparent for customers.